We believe that emerging and frontier markets offer attractive investment opportunities, thanks to long-term trends in demographics, deregulation, offshore outsourcing and improving corporate governance.

Why Emerging Markets and Frontier Markets Now?

We believe the global economy is increasingly splitting into distinct blocs: the “old” economies and the BRICS nations. Key factors including population growth, lower structural debt-to-GDP ratios, and the accelerating trend of de-dollarization, driven in part by the use of economic sanctions, suggest that BRICS economies will continue to rise in prominence. As fiduciaries, it is imperative to evaluate global investment opportunities with objectivity, prioritizing economic realities rather than ideological biases.

Contrary to prevailing concerns, we believe Emerging Markets could perform well during the upcoming Trump administration. Historically, U.S. foreign policy has been assertive from a military perspective. However, we expect the Trump administration to adopt a more business-focused assertiveness. This shift, in our view, introduces new opportunities and challenges for global markets. Many are dismissing President-elect Trump’s recent geopolitical comments, but we take a different perspective. We believe the post-1990 American hegemony period has ended, envisioning a return to global spheres of influence.

Trump’s recent comments about the Panama Canal, Greenland, and even Canada suggest what we interpret as a modern-day return to the core of the U.S. psyche—a contemporary Monroe Doctrine. Before World War II, the U.S. was reluctant to engage in foreign interventions, as reflected in famous quotes such as John Quincy Adams’: “America does not go abroad in search of monsters to destroy,”(1) or George Washington’s: “It is our true policy to steer clear of permanent alliances with any portion of the foreign world.”(2) Perhaps most pertinent to what we perceive as Trump’s vision is Thomas Jefferson’s statement: “Peace, commerce, and honest friendship with all nations—entangling alliances with none.”(3)

We foresee the world separating into spheres of influence. The United States may reassert its Monroe Doctrine oversight of the Western Hemisphere. Europe could see a reshuffle in posture as a revitalized Russia seeks to protect its western frontiers. In Asia, China is likely to dominate its immediate region, encompassing the Yellow Sea, East China Sea, and South China Sea. Meanwhile, a rising India could exert influence over the Indian Ocean region.

This evolving global landscape will pose challenges for certain countries and regions. Europe appears particularly vulnerable. Once-mighty economic powers like Germany now face the consequences of severing ties to cheap, reliable energy sources and adopting antagonistic approaches toward their natural trade partners, especially China and Russia. Traditional export markets for German goods have diminished. Anecdotally, we’ve been informed by close contacts and industry sources(4) that Chinese cars are now appearing on Moscow’s streets at a rapid and abundant pace.

This potentially changing landscape and shifts in realpolitik require investment managers who can anticipate these changes and position themselves and their investors to benefit. We believe Emerging Market managers possess a unique skill set for navigating these evolving times. They have always needed to understand how macro-level shifts impact countries and individual positions at a micro level, a skill set that will become increasingly vital as these shifts accelerate.

- July 4, 1821: Speech to the U.S. House of Representatives on Foreign Policy | Miller Center

- Avalon Project – Washington’s Farewell Address 1796

- The Avalon Project : Jefferson’s First Inaugural Address

- Sales of Chinese Cars Surge in Russia – Lubes’N’Greases

Higher Gross Domestic Product growth rates may help drive profits and returns.

Demographic dividends can drive regional and domestic growth.

Emerging markets offer compelling diversification benefits for long-term investors.

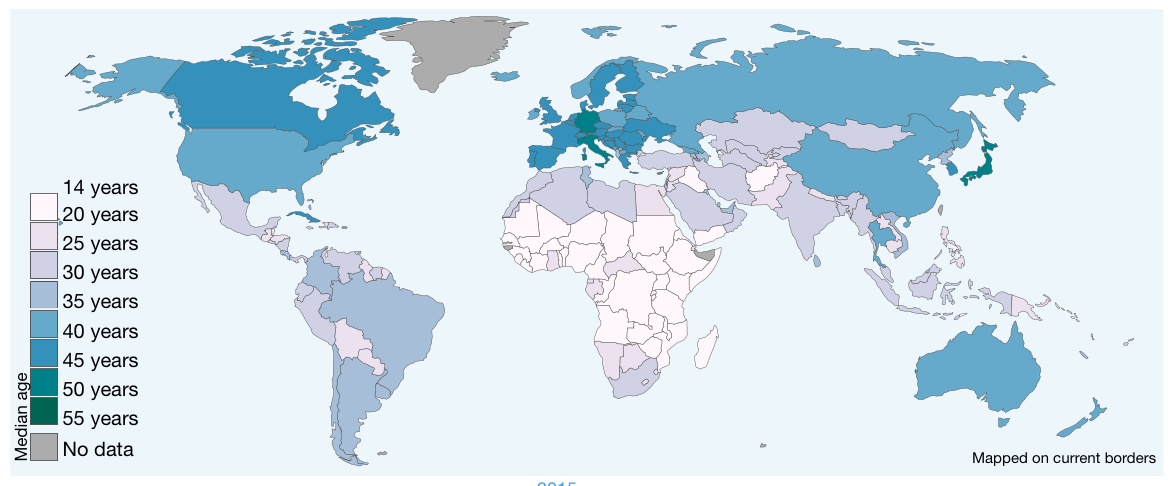

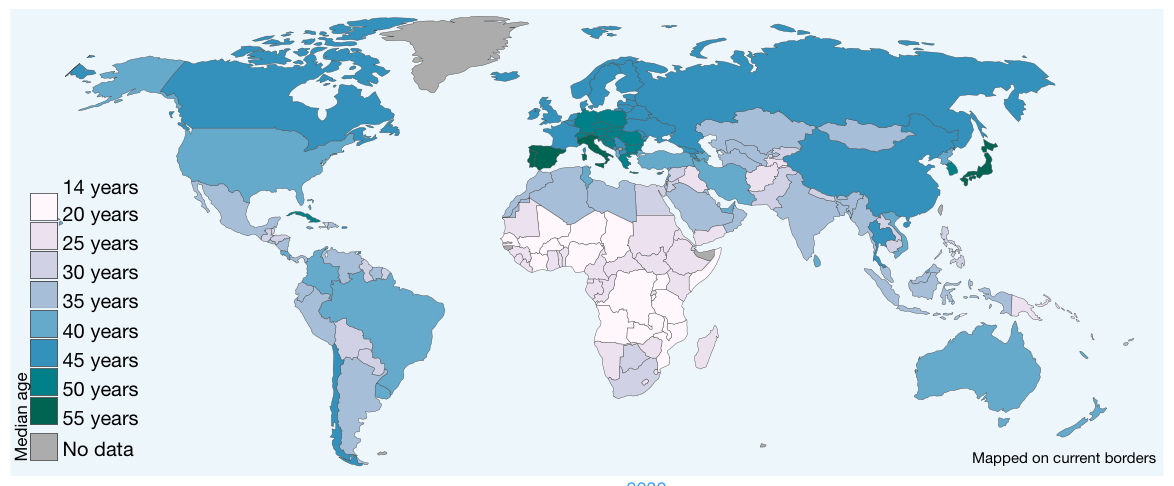

Demographic Dividends May Drive Regional and Domestic Growth.

Median Age, 2015

Much of Africa, Asia, and Latin America have young and growing population.

Median Age, 2030

Larger labor forces as a % of a country’s population can mean greater economic activity, consumption and GDP growth.

*Source UN Population Division (Median Age) 2015 Revision.

Note: 1950 to 2015 show historical estimates. From 2020 the UN projections (medium variant) are shown.

For Illustrative Purposes Only.

Higher Growth Rates May Help Drive Profits and Returns.

| REAL GDP GROWTH (Annual % Change)* |

2023 (Projected) |

|---|---|

| China | 5.5 |

| Vietnam | 6.5 |

| India | 8.2 |

| Indonesia | 5.6 |

| Pakistan | 5.0 |

| United States | 1.4 |

| Euro Area | 1.4 |

| Japan | 0.5 |

*Source ©IMF, 2018, World Economic Outlook (April 2018)

For Illustrative Purposes Only.

© 2021 RVX. Legal Disclaimer